Programmable Money: The Architecture Already Exists

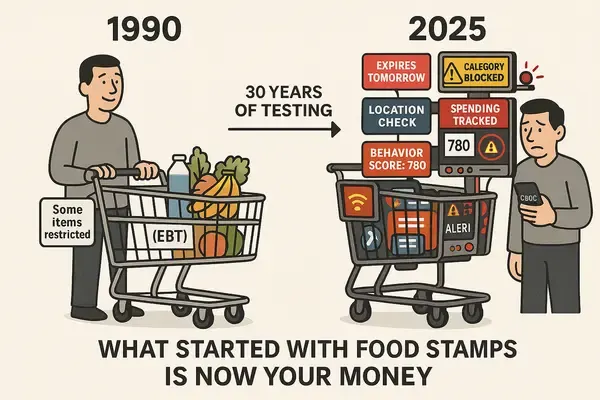

Food stamps weren't welfare—they were a 30-year beta test for programmable money. Now CBDCs deploy that blueprint globally: 130+ countries implementing category restrictions, real-time surveillance, and expiring balances. What was tested on the poor now rolls out to everyone.

last update: FEBRUARY 23, 2026 · Strategic Intelligence

Before any discussion of intent or conspiracy, there is a simpler question: what does the infrastructure actually do?

That question — applied to two separate systems, across a thirty-year gap — produces an answer worth examining carefully.

The first system is SNAP/EBT, the U.S. Supplemental Nutrition Assistance Program. The second is the wave of Central Bank Digital Currency pilots now active in 130+ countries (BIS 2025). The question is not whether one was designed to become the other. The question is: why do they share the same technical feature set?

From welfare administration to monetary architecture — the same control stack, progressively scaled.

These are not interpretations. These are the documented, operational features of SNAP/EBT as deployed across the United States today (USDA FNS 2025a, 2025b):

| Feature | How It Works in SNAP |

|---|---|

| Category Restrictions | Federal law (7 U.S.C. § 2012) defines eligible food items at the category level. Tobacco, alcohol, hot prepared food: excluded by rule, enforced at point-of-sale (USDA FNS 2025a). |

| Merchant Authorization | Retailers must apply to USDA FNS for authorization. Unauthorized merchants cannot accept EBT, regardless of what they sell (USDA FNS 2025b). |

| Real-Time Logging | Every EBT transaction is recorded: timestamp, merchant ID, amount, item category. Stored and auditable by federal agencies indefinitely. |

| Expiring Balances | Most states expire unused SNAP benefits after 274–365 days of account inactivity (USDA FNS 2023). |

| Administrative Override | Accounts can be frozen, suspended, or terminated by agency determination. No judicial order required for administrative holds. |

None of the above is disputed. It is the published, operational design of SNAP — a system currently serving approximately 42 million Americans (USDA FNS 2024).

Same five control capabilities. Thirty years apart. Different stated purpose. Identical architecture (BIS 2025; European Commission 2023; PBoC 2021).

The BIS published its CBDC design handbook (BIS 2025). The digital euro legislative proposal (European Commission 2023) is publicly available. The e-CNY pilot documentation has been studied by the Atlantic Council, CSIS, and the IMF (PBoC 2021). These are not leaks. They are policy documents.

The feature mirror above maps each SNAP capability to its documented CBDC equivalent (BIS 2022; IMF 2022; European Commission 2023). The argument here is not that CBDC architects copied SNAP. The argument is that the same engineering constraints — programmable rules, authorized endpoints, full audit trails, administrative control — were required in both cases. The blueprint was not conspiratorial. It was practical.

Two conclusions are defensible from the data above. One is strong. One is speculative. Cache256 separates them.

STRONG: The technical architecture of SNAP/EBT and the technical architecture of current CBDC proposals are functionally isomorphic. The same five control capabilities appear in both systems. This is documented fact (USDA FNS 2025a; BIS 2025; European Commission 2023).

STRONG: These capabilities — once built into a monetary system — persist. The infrastructure does not disappear when the political conditions that created it change. The feature set becomes available to whoever controls the system.

SPECULATIVE (clearly labeled): That this architecture will be used for broad population control as a deliberate policy objective. Possible. Plausible in adversarial governance contexts. Not proven by the architecture alone.

The distinction matters because conflating the two is precisely what allows critics to dismiss the entire analysis. The architecture argument stands without the intent argument. Focus there.

The Kraken × Citadel Securities deal (Nov 2025) fits this frame, but requires its own precision (Kraken 2025; Fortune 2025).

Citadel Securities is not a passive investor. It is a market-making infrastructure company operating under SEC and FINRA oversight, with documented KYC/AML obligations extending to its counterparties. When a firm of that profile takes a strategic stake in a crypto exchange, the compliance architecture of the investor necessarily shapes the operational constraints of the target.

This is not a claim of bad faith by either party. It is a structural observation: regulated capital has regulatory obligations that travel with it. The Kraken deal is one data point in a pattern of TradFi integration that includes BlackRock's BUIDL fund, Fidelity's crypto custody expansion, and the general migration of institutional on-ramps toward SAB 121-compliant custody frameworks.

The question is not whether these actors are hostile to crypto. The question is: what does their presence do to the censorship-resistance properties of the rails they control?

Every control capability requires a surface to enforce against. Shielded transactions remove that surface at the cryptographic level — not by policy, but by design.

Note: "no enforcement surface" applies only to on-chain transactions between shielded addresses. On-ramp and off-ramp points (exchanges, fiat conversion) remain subject to KYC/AML regardless of shielding. The privacy guarantee is transaction-layer only.

Against the feature set described above, Zcash's fully shielded transactions (zs1… addresses, Orchard pool) are notable not for ideological reasons but for architectural ones. As shown in the control surface diagram above, fully shielded ZEC transactions expose no sender, receiver, amount, or linkage data.

This means the control features described in sections 2 and 3 — category rules, merchant authorization, audit trail, override — have no enforcement surface on shielded ZEC. Not because of any legal protection. Because of the cryptographic structure of the transaction itself.

Note (2026): The Zcash Foundation and several key contributors announced their progressive withdrawal in 2024–2025. This does not invalidate the cryptographic property of shielded transactions (zk-SNARKs), but significantly reduces the likelihood of active maintenance, upgrades, and large-scale future adoption. The rail remains technically operational as long as the network exists, but its practical viability is declining.

The practical window for low-friction access to this rail is narrowing on two fronts: on-ramp KYC requirements continue to tighten globally (FATF Travel Rule implementation, MiCA Art. 68), and regulatory pressure on privacy coins has accelerated following the Tornado Cash precedent (2022). Whether that window closes in 12 months or 48 is an estimate, not a fact. But the direction of regulatory travel is not ambiguous.

The programmable money architecture is not a future threat. It is a present reality — documented in policy papers, CBDC pilot reports, and three decades of SNAP operational data. The infrastructure exists. The capabilities are built.

What happens next depends on governance decisions that have not yet been made in most jurisdictions. That uncertainty is real, and it matters. But the infrastructure argument does not require the worst-case governance scenario to be valid.

The operative question for anyone who values financial autonomy is not whether the architecture exists. It is: what rails are you using, and what does the entity controlling those rails have the technical ability to do?

Answering that question — clearly, without inflation — is what Cache256 is for.

→ Food Stamps: The Programmable Money Blueprint (Aug 2025)

→ Kraken × Citadel: CEX Capture Analysis (Nov 2025)

→ Zcash Privacy Layer: zk-SNARKs Architecture (Nov 2025)

→ CBDCs: The Control Layer (Jun 2025)

→ All Sovereignty Intelligence

References

BIS (Bank for International Settlements) (2022) Building regional payment areas: the single rule book approach. BIS Working Papers No 1016. Basel: BIS. Available at: https://www.bis.org/publ/work1016.pdf (Accessed: 23 February 2026).

BIS (Bank for International Settlements) (2025) Central bank digital currencies: design handbook. Basel: BIS. (Updated edition).

European Commission (2023) Proposal for a regulation of the European Parliament and of the Council on the establishment of the digital euro. COM(2023) 369 final. Brussels: European Commission. Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML?uri=CELEX%3A52023PC0369 (Accessed: 23 February 2026).

IMF (International Monetary Fund) (2022) Behind the scenes of central bank digital currency. IMF Staff Discussion Note SDN/22/03. Washington, DC: IMF.

Kraken (2025) Kraken raises $800 million to advance strategic roadmap. Kraken Blog, 18 November. Available at: https://blog.kraken.com/news/800-million-raise-to-advance-strategic-roadmap (Accessed: 23 February 2026).

PBoC (People's Bank of China) (2021) Progress of research & development of e-CNY in China. White Paper. Beijing: PBoC. Available at: https://www.pbc.gov.cn/en/3688110/3688172/4157443/4293696/2021071614584691871.pdf (Accessed: 23 February 2026).

USDA FNS (United States Department of Agriculture Food and Nutrition Service) (2023) SNAP policy on expiring balances. Washington, DC: USDA FNS.

USDA FNS (United States Department of Agriculture Food and Nutrition Service) (2025a) What can SNAP buy? Washington, DC: USDA FNS. Available at: https://www.fns.usda.gov/snap/eligible-food-items (Accessed: 23 February 2026).

USDA FNS (United States Department of Agriculture Food and Nutrition Service) (2025b) Store eligibility requirements. Washington, DC: USDA FNS. Available at: https://www.fns.usda.gov/snap/retailer/eligible (Accessed: 23 February 2026).

Fortune (2025) Crypto exchange Kraken raises $200 million from Ken Griffin's Citadel. Fortune, 18 November. Available at: https://fortune.com/2025/11/18/kraken-citadel-securities-ken-griffin-800-million-fundraise (Accessed: 23 February 2026).